WE LIVE in an age of “emergencies”: a climate emergency, a cost-of-living emergency and, in Scotland since May 2024, a housing emergency. The word can be overused, but in the case of housing there is a real problem — particularly for young people trying to get on the property ladder.

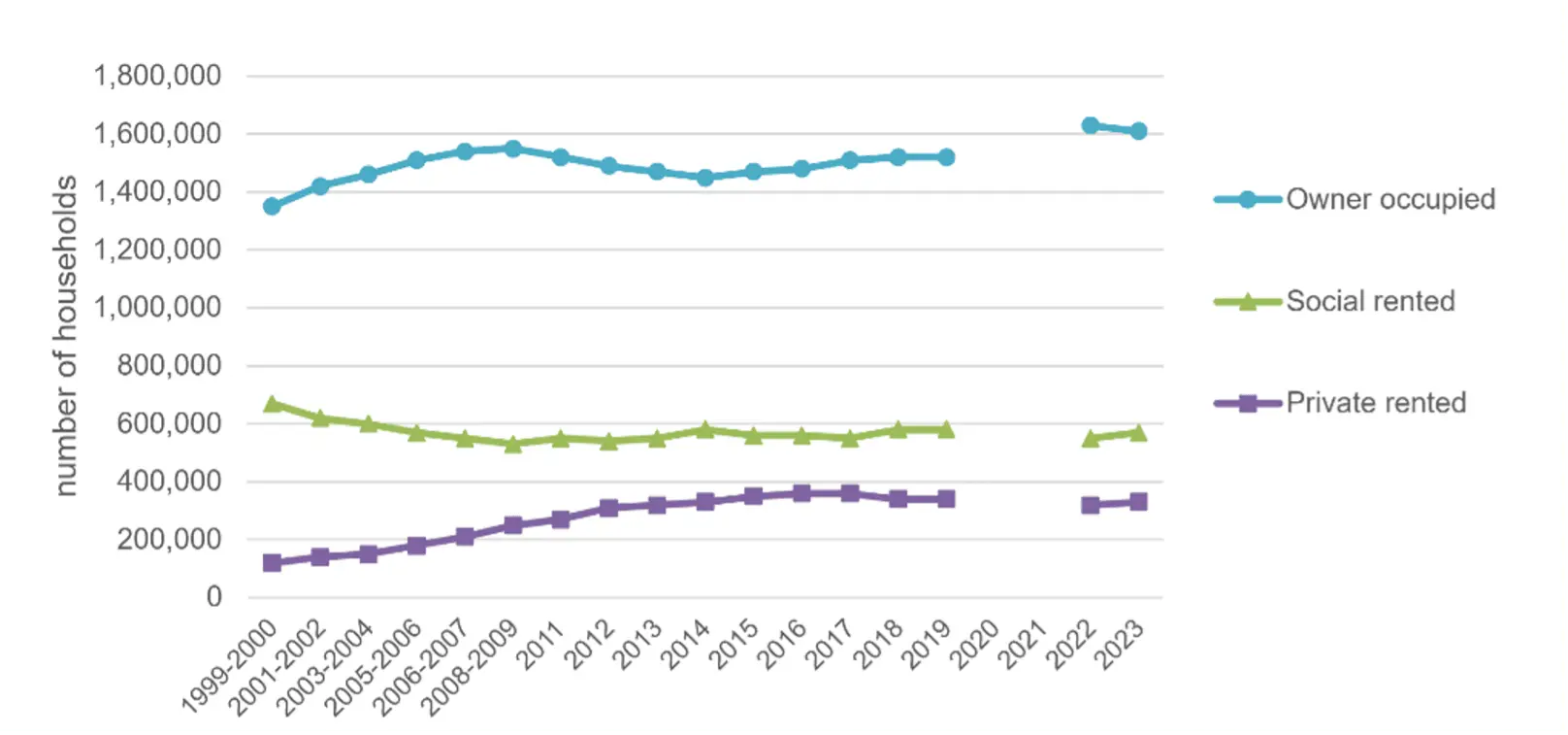

Scotland has around 2.5 million homes. Of these, approximately 63% are owner-occupied, either outright or with a mortgage. Almost a quarter are social housing, and around one in seven are privately rented.

Since the turn of the millennium, the proportion of privately rented homes has nearly doubled, while the share of social housing has declined slightly. However, this belies a more recent shift: the private rented sector peaked in 2017 and has since fallen back marginally.

Overall, Scottish home ownership has remained broadly stable, down just one percentage point over the past 25 years, and closely mirrors ownership levels across the UK.

Scottish housing stock – estimates of ownership type

However, there is undoubtedly a serious problem. At the sharp end, far too many people are living in temporary accommodation. According to the Scottish Government, 17,000 households are in that predicament — a rise of 6 per cent over the year. Worse still, 34,067 households were assessed by councils as homeless, the highest figure on record.

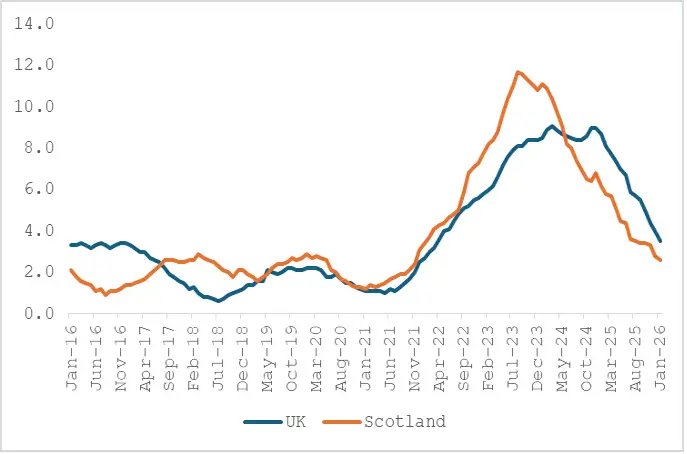

This is only the tip of the iceberg. Rents are high and, as the chart below shows, the cost of renting has often risen faster than inflation. According to the ONS, the average monthly private rent in Scotland is now £1,021, up 2.5 per cent over the year.

Comparing average rents with median monthly pay — estimated by the Scottish Government at £2,580 — highlights the scale of the problem. While comparing averages can be misleading, current rents amount to almost 40 per cent of median earnings, suggesting significant financial stress for many households.

Worse, it risks creating a culture of dependency, as the chances of saving enough for a deposit are slim when so much income is absorbed by tax and rent. Little is left to build meaningful savings for a first home. This creates a vicious circle that undermines intergenerational opportunity. So we can agree: there is a problem.

Key nation fiscal deficit % GDP 2000

The question is: why has this occurred and why has it become more acute? And — if blame is to be apportioned — where does it lie?

There is no single explanation, and no magic bullet. However, the answer is not simply greedy landlords or exploitation. It is more accurately described as market failure. The evidence overwhelmingly suggests that this failure is the cumulative result of incremental actions taken over many years by politicians, regulators and central bankers in both the UK and Scotland. Through sustained interference with market mechanisms, they have contributed directly to higher house prices and very elevated private rents.

In a true — properly functioning —market, both house prices and rents would likely be much more affordable. The irony is that as the Scottish Government and others declare a “housing emergency” and wallow in sanctimony, they are to a significant extent the architects of the very crisis they lament.

So why is this so? Surely it is the nasty landlords who done it? No. The primary responsibility lies with policymakers — politicians, central bankers and regulators — whose actions have had incremental but powerful effects.

In my view, the principal factors are the impact of quantitative easing and a decade of central bank monetary repression, planning constraints, unplanned migration flows, banking and credit regulation, net zero, regulation and increased property taxation. If this assessment is correct, the problem rests largely with government rather than the private sector.

The single most significant factor, in my view, was the action of central bank policy following the Global Financial Crisis. In response to the banking collapse — itself arguably the result of regulation and political interferences in the lending processes in the US — central banks printed money and slashed interest rates to near zero for over a decade. Although that era has now ended, its aftershocks remain.

One of the primary impacts of this policy was to push up asset prices, particularly property. Quantitative easing and the Bank of England’s ‘free cost of money” approach undoubtedly puffed up property prices materially. Had market forces been allowed to operate more freely after the GFC, property prices would likely have fallen substantially.

Maintaining a near-zero interest rate policy for over a decade after the GFC was an act of folly: it greatly distorted the market to the detriment of those without assets, especially the young. In a nut shell, it created arbitrary winners and losers. Those with debt and assets were bailed out; those starting out and hoping to get on the property ladder found it increasingly difficult.

Allied to this, a post-crisis tightening of banking regulation made it harder to lend to certain groups. While intended to reduce the risk of a future banking crisis, the result was that for many it became easier to secure a buy-to-let mortgage than a first residential mortgage. This further skewed the market against first-time buyers.

Migration has also been a significant factor. If demand increases while housing supply remains relatively static, prices and rents will rise. This is not rocket science. The law holds for apples, pears and houses.

The UK has seen migration flows averaging in excess of 500,000 each year since 2000. Housebuilding has not remotely kept pace with population growth. Pressure has fallen disproportionately on the private and social rented sectors, intensifying supply-demand imbalances.

Initially, Scotland was less affected, as many migrants settled in London and parts of England. However, that has changed in recent years, placing significant strain on Glasgow and parts of Edinburgh. The political denial of this link is deafening.

Next in the hall of shame are regulation and net zero. Over the past two decades, the degree of regulation in the rental sector has increased exponentially in numerous ways from enhanced tenant rights, inspection requirements certification obligations, taxation changes and increasingly demanding environmental standards.

Basic economics suggests that when landlords face higher compliance costs, those costs are often passed on to tenants. The Climate Change Committee has estimated that meeting net zero targets could require £37 billion of investment in buildings by 2045. Even if a modest proportion of that falls on private landlords, the impact can only be inflationary and materially so.

A final structural constraint is the planning system. It can take years to move from concept to spade, with outcomes varying widely by region. Delays, uncertainty and inconsistent decision-making all restrict supply. A system that takes years to approve developments clearly needs shaking up.

cumulative effect of these policies has been substantial. House prices have risen, rental costs have increased and the path to ownership has narrowed. The result is a vicious circle that makes it progressively harder for the next generation to buy a home.

Property ownership remains central to a free society. It fosters independence, responsibility and long-term security. If the policy errors of the past two decades are not addressed, the prospects for the next generation will remain constrained. Do we really want “generation rent” to become the permanent norm?

The answer is not more regulation, higher property taxes or further planning delays. Each of these measures will only make matters worse. They risk reducing supply and increasing costs, with the burden ultimately falling on tenants. Rent controls and ever-expanding tenant protections, while well-intentioned, will exacerbate shortages if they discourage investment.

There is no quick fix. This situation has developed over 25 years. But progress requires a clear understanding of the underlying causes and a willingness to unwind accumulated policy distortions.

A good government would base its monetary policy on market neutrality, not monetary suppression. It would understand the link between migration flows and housing stock and it would restore regulatory balance. Planning reform must accelerate supply. Scrapping the need for expensive retrofit to meet arbitrary net zero targets would be a good beginning. Banking regulation should be appraised so that lenders could renew their historic role in enabling prudent lending to first-time buyers.

Above all, the next generation needs hope. Generation rent is being hamstrung by very high rents, very high tax and hefty student debt. Much of this pressure stems from political choices. It can and must be undone if the next generation is to have much hope.

Comments: 0

Join the debate

Do you agree with this analysis, or is the author wrong? Have your say below.

No comments yet. Be the first to join the discussion.